All of our content is based on objective analysis, and the opinions are our own. The model can also decide whether or not it is more beneficial for one company to acquire another or if it would make sense for both businesses to merge. Since the total present value or DCF is less than the cost of the investment, we can conclude that the investment is not worthwhile. Net Present Value (NPV) is the difference between the initial cost of an investment and its present value.

Best Corporate Finance Books to Get You Started in 2024

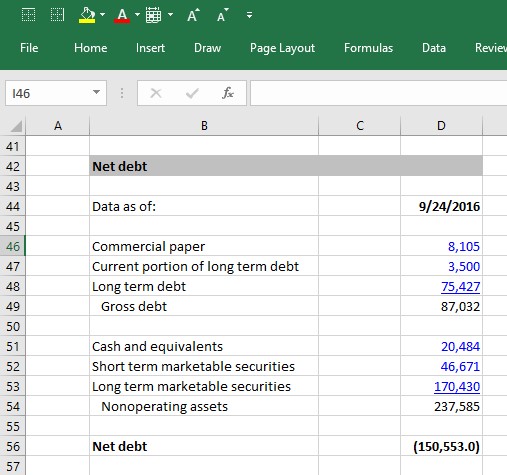

As mentioned earlier, enterprise value is the value of thebusiness as a whole. To get the equity value, we need to deduct the debt value(because it belongs to the debt holder). You can get the debt value from thebalance sheet of the business (sum of all borrowings) as of the valuation date.In our example, we assume the company has $50k debt. However, due to difficulties of doing a normalization of cashflow with the H-Model, I would suggest you to extend the forecast period toconsider the high growth period instead of using the H-model. Given net profit has already deducted finance cost, to compute the FCFF, we need to add back the finance cost as illustrated below.

DCF Model, Step 3: The Terminal Value

If fixed assets depreciate faster then your capital expenditure, then in the long-term, there will be no fixed assets left in the business which doesn’t make sense for a going concern. Most valuation specialists, normalize terminal year capital expenditure by making equal to D&A. For example, start-up businesses have high growth expectations and should incorporate a longer projection period as compared to a mature business. That being said, since we cannot predict the future, most forecasts typically go up to 3-years or 5-years. Some businesses may be able to forecast more accurately for even longer periods (say 10 years) because they have more predictable cashflows which could be due to signed agreements/concessions. DCF calculators are indispensable for investors seeking to make data-driven decisions.

Applicable to a Wide Variety of Investments, Projects, or Companies

In this interest-rate environment, executives and investors alike are being forced to make tough decisions about where to put their money. To forecast accurately, break your projections into short-term (typically 5 years) and long-term (terminal value) time frames. Many analysts use financial tools like Discounted Cash Flow Reports APIs to get projections and automate part of this process, making it more efficient. Get instant access to video lessons taught by experienced investment bankers. Learn financial statement modeling, DCF, M&A, LBO, Comps and Excel shortcuts. The Risk-Free Rate (RFR) is what you might earn on “safe” government bonds in the same currency as the company’s cash flows (so, U.S. Treasuries here).

GAAP aren’t too bad because U.S. companies still record Rent as a simple operating expense on their Income Statements. The company’s annual report and investor presentations are the best starting points. The company is also worth less when it is riskier or when expectations for it are higher, i.e., when the Discount Rate is higher. Alternatively, our team of valuation experts is also available to help you by providing a wide range of services. We charge a reasonable and transparent price and you can have a look at what we can offer here.

- Of course, it’s also a bit more complicated than that… To answer this interview question in more detail, we’ve broken it down into several basic steps below.

- A company planning an exit back in, say, 2018 would certainly not have expected that—and yet, that shift can dramatically change the math on discounted cash flow analysis.

- This guide is quite detailed, but it stops short of all corner cases and nuances of a fully-fledged DCF model.

- One place where the book value-as-proxy-for-market-value can be dangerous is with “non-controlling interests.” Non-controlling interests are usually understated on the balance sheet.

- A DCF model estimates a company’s intrinsic value (the value based on a company’s ability to generate cash flows) and is often presented in comparison to the company’s market value.

- For instance, if a firm is investing resources in order to meet the needs of a 3-year contract, they would use a 3-year forecast period.

Step 3: Choose an Appropriate Discount Rate

Using one of these two methods, determine the company’s terminal value so that we can adequately discount cash flows. The discount rate represents the investment’s cost of capital or the minimum acceptable rate of return. If the discounted cash flow is higher than the current cost of the investment, the investment opportunity could be worthwhile. DCF modeling is built on future cash flows, which must be estimated in most cases.

Always be sure to gather accurate data, use a reasonable discount rate, and test different scenarios to get a complete picture. This absence of control reduces the value of the minority equityposition against the total value of the company. Getting the discount rate (WACC in this case) is another dcf model steps topic of its own and we generally estimate the WACC of a business using the CAPM model with reference to market data of listed comparable companies. For terminal year capital expenditure, please note it should always be slightly higher or at least equal to the Depreciation (D&A) expense.

Discounted cash flow (DCF) analysis is a method used in corporate finance and valuation to estimate the attractiveness of an investment opportunity. DCF analysis uses future free cash flow projections and discounts them to arrive at a present value estimate, which is used to evaluate the potential for investment. Discounted cash flow and net present value are not the same, though the two are closely related.